If you have spent any amount of time reading equity research reports from the various brokerage houses (including those that are supplied by your online broker - ICICI Direct, HDFC Sec, etc), you would have come across their stock target prices, and their buy/ sell calls based on those target prices.

Invariably these target prices are calculated based on some variation of Discounted Cash flow, or relative valuation methodologies like P/E, P/B etc. In a shift from the 'target price' model of equity research, Morningstar.com (U.S. site), has inverted this methodology and instead publishes its estimate of intrinsic value and provides its views on stocks based on how much lower or higher than intrinsic value the stocks are trading. The website refrains from publishing target prices.

For value investors, I believe that this is a very sensible approach. Given that the markets are highly unpredictable, it is quite clear that the 'Target Price' based approach might be more suitable for Growth investors as well as investors with shorter time horizons. Typically equity research reports have target horizons of 1 year.

The Morningstar approach works by providing an appraisal of the Intrinsic Value. Investors can then choose to enter or avoid the stock depending on their preference for margin of safety. i.e. Those who would like to invest in deep value situations, might prefer to invest in stocks which are trading at 50% discount to intrinsic value, and so on.

In India, we know Morningstar as a provider of research on Mutual Funds. In the US, the company has progressed and is now actively involved in equity research. I believe that as and when they bring their Intrinsic Value approach to India, it would be a valuable tool for Indian investors.

![Indian Value Investors [IVI]](https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEjl7pfvAzCJ1cY47AEwQ6mf1a6f2a_45X5gbTxfyrbX8T45bNDm7jKKhMqx1zRFI6qxRZ4dgz-_6Ghyphenhyphensx3BWIlVaklI7i6yCyPZOBlPoLwlM18iUKU8eRI13PVls9ldWt6WD0MqEROIT6VT/s1600-r/Bargain+Stocks.jpg)

Click the picture below to access parent website : www.hbjcapital.com / www.hbjcapital.in

Call : 09886736791 / 9677088836 (Multibagger) / 9818866676 (Penny) / 9886403791 (Trading)

Monday, August 25, 2008

Monday, August 11, 2008

Performance of Value Investing in India

Outlook Profit magazine has a wonderful story on the long term results of investors practicing value investing in India. The article features interviews with well known Indian value investors, as well as results of hypothetical value investing portfolios back-tested for their performance since the year 1998.

It is available at: http://www.manualofideas.com/files/content/2008_mahalakshmi.pdf

The article covers several Benjamin Graham strategies to examine their performance over this 10 year period. These include - Cash Bargains, Low P/E (or high earnings yield), etc. Another important contribution of this article is to shine the spotlight on many under-the-radar investors like Prof. Sanjay Bakshi, Chetan Parikh, etc who donot receive much coverage in the business media, but have been generating market beating returns for years and years.

Kudos to the magazine for bringing out such a well researched piece on value investing in India. The article has also accepted into the archive of the Heilbrunn Centre for Value Investing at Columbia Graduate School of Business, the birthplace of Value Investing.

More wonderful value investment related material available at: http://www4.gsb.columbia.edu/valueinvesting/schlossarchives/public

It is available at: http://www.manualofideas.com/files/content/2008_mahalakshmi.pdf

The article covers several Benjamin Graham strategies to examine their performance over this 10 year period. These include - Cash Bargains, Low P/E (or high earnings yield), etc. Another important contribution of this article is to shine the spotlight on many under-the-radar investors like Prof. Sanjay Bakshi, Chetan Parikh, etc who donot receive much coverage in the business media, but have been generating market beating returns for years and years.

Kudos to the magazine for bringing out such a well researched piece on value investing in India. The article has also accepted into the archive of the Heilbrunn Centre for Value Investing at Columbia Graduate School of Business, the birthplace of Value Investing.

More wonderful value investment related material available at: http://www4.gsb.columbia.edu/valueinvesting/schlossarchives/public

Friday, August 8, 2008

Behavioural Investing: Anchoring

A building needs to be be built on a solid foundation, a theory must be built on solid arguments, and an investment decision must be built on solid analysis. However, investors often make investment decisions which are built not on solid analysis, but "anchored" on reference point. How does this impact returns enjoyed by investors? In the following paragraphs, we investigate.

Imagine that Mr. A purchased stock in company 'A' for Rs 100 per share. The stock steadily rises to Rs 150 over a period of a year. Unfortunately, as it turns out, the company derives 50% of its sales from its license of a fast-selling software product. Suddenly, the licensor decides to withdraw the license and enter the market on its own. The stock tanks as soon as the news breaks and hits 110. However, Mr. A sees that the stock is off its high of 150 and hence erroneously assumes it is undervalued, and purchases more stocks.

However, the company's fundamentals have clearly deteriorated, with no immediate hope of maintaining its earnings, unless it is able to take some radical steps. Thus, by falling victim to 'Anchoring Bias', Mr. A has compounded his loss.

Anchoring also works in another way. Since, even at Rs 110, the stock is above Mr. A's purchase price, he still has an illusory feeling that he is in the money. Hence, he continues to hold/ or even increases his position in the stock. Thus, instead of redeploying his money in a company with better fundamentals, he is continues to suffer from the consequences of his behavioural biases.

Imagine that Mr. A purchased stock in company 'A' for Rs 100 per share. The stock steadily rises to Rs 150 over a period of a year. Unfortunately, as it turns out, the company derives 50% of its sales from its license of a fast-selling software product. Suddenly, the licensor decides to withdraw the license and enter the market on its own. The stock tanks as soon as the news breaks and hits 110. However, Mr. A sees that the stock is off its high of 150 and hence erroneously assumes it is undervalued, and purchases more stocks.

However, the company's fundamentals have clearly deteriorated, with no immediate hope of maintaining its earnings, unless it is able to take some radical steps. Thus, by falling victim to 'Anchoring Bias', Mr. A has compounded his loss.

Anchoring also works in another way. Since, even at Rs 110, the stock is above Mr. A's purchase price, he still has an illusory feeling that he is in the money. Hence, he continues to hold/ or even increases his position in the stock. Thus, instead of redeploying his money in a company with better fundamentals, he is continues to suffer from the consequences of his behavioural biases.

Thursday, July 24, 2008

The Futility of Trying to Predict The Market

Everyday, investors are exposed to the writings and speeches of numerous 'experts' and analysts who give their predictions regarding where they foresee the market over the next 1/6/12 months, etc. Based on their comments, many investors decide whether to invest further or whether to book profits and stay out of the market for a while. Since, no one really has a crystal ball helping them to predict exact market movements, it is important for value investors to treat these predictions with a pinch of salt.

The world's greatest investors usually try to shy away from giving predictions regarding the market, except to give general statements and predictions with longer horizons in mind.

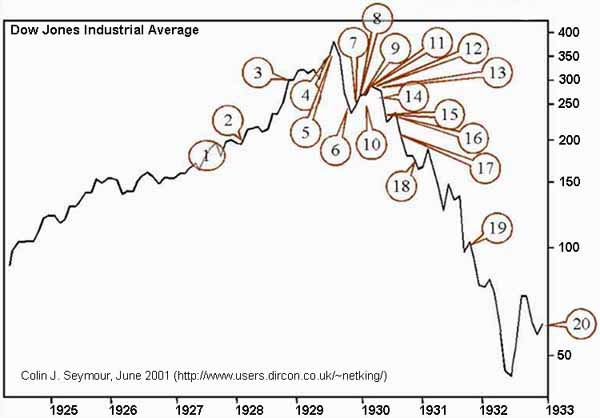

The following is an interesting look at the statements of the best and brightest experts and economists during the Great Depression of 1929. It is amusing to see how wrong their statements proved to be in hindsight. This further underscores the importance of not trying to predict market movements and instead to identify good companies trading at sufficient margins of safety to their real value.

Courtesy Colin Seymour

The world's greatest investors usually try to shy away from giving predictions regarding the market, except to give general statements and predictions with longer horizons in mind.

The following is an interesting look at the statements of the best and brightest experts and economists during the Great Depression of 1929. It is amusing to see how wrong their statements proved to be in hindsight. This further underscores the importance of not trying to predict market movements and instead to identify good companies trading at sufficient margins of safety to their real value.

Courtesy Colin Seymour

For relvance to 2001, scroll down to "Fast forward"

1.

"We will not have any more crashes in our time."

- John Maynard Keynes in 1927 [NB: The authenticity of this one is a little suspect]

2.

"I cannot help but raise a dissenting voice to statements that we are living in a fool's paradise, and that prosperity in this country must necessarily diminish and recede in the near future."

- E. H. H. Simmons, President, New York Stock Exchange, January 12, 1928"There will be no interruption of our permanent prosperity."

- Myron E. Forbes, President, Pierce Arrow Motor Car Co., January 12, 1928

3.

"No Congress of the United States ever assembled, on surveying the state of the Union, has met with a more pleasing prospect than that which appears at the present time. In the domestic field there is tranquility and contentment...and the highest record of years of prosperity. In the foreign field there is peace, the goodwill which comes from mutual understanding."

- Calvin Coolidge December 4, 1928

4.

"There may be a recession in stock prices, but not anything in the nature of a crash."

- Irving Fisher, leading U.S. economist, New York Times, Sept. 5, 1929

5.

"Stock prices have reached what looks like a permanently high plateau. I do not feel there will be soon if ever a 50 or 60 point break from present levels, such as (bears) have predicted. I expect to see the stock market a good deal higher within a few months."

- Irving Fisher, Ph.D. in economics, Oct. 17, 1929"This crash is not going to have much effect on business."

- Arthur Reynolds, Chairman of Continental Illinois Bank of Chicago, October 24, 1929"There will be no repetition of the break of yesterday... I have no fear of another comparable decline."

- Arthur W. Loasby (President of the Equitable Trust Company), quoted in NYT, Friday, October 25, 1929"We feel that fundamentally Wall Street is sound, and that for people who can afford to pay for them outright, good stocks are cheap at these prices."

- Goodbody and Company market-letter quoted in The New York Times, Friday, October 25, 1929

6.

"This is the time to buy stocks. This is the time to recall the words of the late J. P. Morgan... that any man who is bearish on America will go broke. Within a few days there is likely to be a bear panic rather than a bull panic. Many of the low prices as a result of this hysterical selling are not likely to be reached again in many years."

- R. W. McNeel, market analyst, as quoted in the New York Herald Tribune, October 30, 1929"Buying of sound, seasoned issues now will not be regretted"

- E. A. Pearce market letter quoted in the New York Herald Tribune, October 30, 1929"Some pretty intelligent people are now buying stocks... Unless we are to have a panic -- which no one seriously believes, stocks have hit bottom."

- R. W. McNeal, financial analyst in October 1929

7.

"The decline is in paper values, not in tangible goods and services...America is now in the eighth year of prosperity as commercially defined. The former great periods of prosperity in America averaged eleven years. On this basis we now have three more years to go before the tailspin."

- Stuart Chase (American economist and author), NY Herald Tribune, November 1, 1929"Hysteria has now disappeared from Wall Street."

- The Times of London, November 2, 1929"The Wall Street crash doesn't mean that there will be any general or serious business depression... For six years American business has been diverting a substantial part of its attention, its energies and its resources on the speculative game... Now that irrelevant, alien and hazardous adventure is over. Business has come home again, back to its job, providentially unscathed, sound in wind and limb, financially stronger than ever before."

- Business Week, November 2, 1929"...despite its severity, we believe that the slump in stock prices will prove an intermediate movement and not the precursor of a business depression such as would entail prolonged further liquidation..."

- Harvard Economic Society (HES), November 2, 1929

8.

"... a serious depression seems improbable; [we expect] recovery of business next spring, with further improvement in the fall."

- HES, November 10, 1929"The end of the decline of the Stock Market will probably not be long, only a few more days at most."

- Irving Fisher, Professor of Economics at Yale University, November 14, 1929"In most of the cities and towns of this country, this Wall Street panic will have no effect."

- Paul Block (President of the Block newspaper chain), editorial, November 15, 1929"Financial storm definitely passed."

- Bernard Baruch, cablegram to Winston Churchill, November 15, 1929

9.

"I see nothing in the present situation that is either menacing or warrants pessimism... I have every confidence that there will be a revival of activity in the spring, and that during this coming year the country will make steady progress."

- Andrew W. Mellon, U.S. Secretary of the Treasury December 31, 1929"I am convinced that through these measures we have reestablished confidence."

- Herbert Hoover, December 1929"[1930 will be] a splendid employment year."

- U.S. Dept. of Labor, New Year's Forecast, December 1929

10.

"For the immediate future, at least, the outlook (stocks) is bright."

- Irving Fisher, Ph.D. in Economics, in early 1930

11.

"...there are indications that the severest phase of the recession is over..."

- Harvard Economic Society (HES) Jan 18, 1930

12.

"There is nothing in the situation to be disturbed about."

- Secretary of the Treasury Andrew Mellon, Feb 1930

13.

"The spring of 1930 marks the end of a period of grave concern...American business is steadily coming back to a normal level of prosperity."

- Julius Barnes, head of Hoover's National Business Survey Conference, Mar 16, 1930"... the outlook continues favorable..."

- HES Mar 29, 1930

14.

"... the outlook is favorable..."

- HES Apr 19, 1930

15.

"While the crash only took place six months ago, I am convinced we have now passed through the worst -- and with continued unity of effort we shall rapidly recover. There has been no significant bank or industrial failure. That danger, too, is safely behind us."

- Herbert Hoover, President of the United States, May 1, 1930"...by May or June the spring recovery forecast in our letters of last December and November should clearly be apparent..."

- HES May 17, 1930"Gentleman, you have come sixty days too late. The depression is over."

- Herbert Hoover, responding to a delegation requesting a public works program to help speed the recovery, June 1930

16.

"... irregular and conflicting movements of business should soon give way to a sustained recovery..."

- HES June 28, 1930

17.

"... the present depression has about spent its force..."

- HES, Aug 30, 1930

18.

"We are now near the end of the declining phase of the depression."

- HES Nov 15, 1930

19.

"Stabilization at [present] levels is clearly possible."

- HES Oct 31, 1931

20.

"All safe deposit boxes in banks or financial institutions have been sealed... and may only be opened in the presence of an agent of the I.R.S."

- President F.D. Roosevelt, 1933

Fast forward... year 2001

Thursday, July 17, 2008

When to Sell a Stock

Many investors buy stocks with pre-defined sell triggers in mind. "I'll sell the stock in 1 year", "I'll sell the stock once it gives me a 50% return", "I'll sell it when it once the current acquisition plan is finalised", etc.

Value investors, however, look at selling stock holdings in a very different way. To value investors, there are only 3 reasons to sell stocks:

1. The valuation becomes too expensive. eg: the stock was trading at a P/E of 10 at the time of purchase. After 2 years of patient holding, the stock has now reached P/E of 20, which is much higher than the historical average for the company, as well as higher than the industry average. Time to Sell!

2. The original investment case is no longer valid. eg: Mr. A invests in a stock in the real estate industry, because he believes that the then benign interest rate scenario is very favourable for the real estate industry. However, the rate cycle eventually turns and rates end up becoming high enough to begin to hit real estate sales. Clearly, the original investment case (Low interest rates = good time for real estate stocks) is no longer valid. Time to Sell!

3. A better opportunity comes along. eg: Mr. A decides to invest in an auto stock because he believes that as India's middle class gets higher disposable incomes, the demand for automobiles is going to rise exponentially. However, after looking at the value chain of the auto industry, he feels (rightly or wrongly) that rather than the auto manufacturers, certain auto component manufacturers are the ones who are actually cornering most of the profit margins in the industry's growth. Time to exit auto & enter auto components.

Value investors, however, look at selling stock holdings in a very different way. To value investors, there are only 3 reasons to sell stocks:

1. The valuation becomes too expensive. eg: the stock was trading at a P/E of 10 at the time of purchase. After 2 years of patient holding, the stock has now reached P/E of 20, which is much higher than the historical average for the company, as well as higher than the industry average. Time to Sell!

2. The original investment case is no longer valid. eg: Mr. A invests in a stock in the real estate industry, because he believes that the then benign interest rate scenario is very favourable for the real estate industry. However, the rate cycle eventually turns and rates end up becoming high enough to begin to hit real estate sales. Clearly, the original investment case (Low interest rates = good time for real estate stocks) is no longer valid. Time to Sell!

3. A better opportunity comes along. eg: Mr. A decides to invest in an auto stock because he believes that as India's middle class gets higher disposable incomes, the demand for automobiles is going to rise exponentially. However, after looking at the value chain of the auto industry, he feels (rightly or wrongly) that rather than the auto manufacturers, certain auto component manufacturers are the ones who are actually cornering most of the profit margins in the industry's growth. Time to exit auto & enter auto components.

Tuesday, July 8, 2008

Prospect Theory

Prospect Theory is the foundation of the field of economics and finance which has now become popular as Behavioural Economics/ Behavioural Finance.

Economists Daniel Kahneman and Amos Tversky developed the concept of Prospect Theory in 1979 after an empirical study of the how individuals choose between alternatives in the presence of risk. Prospect Theory is a very useful framework to describe how investors respond to gains and losses in the markets. In the most simplistic form, prospect theory can be described by the function shown in the graph above. It states that the pain felt by individuals when they incur losses is twice the pleasure felt when they secure gains.

Prospect Theory is a very useful framework to describe how investors respond to gains and losses in the markets. In the most simplistic form, prospect theory can be described by the function shown in the graph above. It states that the pain felt by individuals when they incur losses is twice the pleasure felt when they secure gains.

Applied to the field of investing, the theory states that investors value gains and losses differently, i.e. the emotional impact of losses is much higher than the emotional high of gains.

When it was formulated, Prospect Theory was completely against the prevailing consensus of the time, viz. economic agents are rational and treat losses and gains equally, and try to maximise their potential gains in all decision making. Prospect theory states that the emotional impact of potential losses causes significant changes in investor behaviour and thus affects decisions to buy and sell, and hence future returns.

Further research based on Prospect Theory has revealed a number of behavioural biases, which affect economic returns. We shall cover some of these in future posts. An awareness of these biases will help to prevent very obvious errors in investing, such as Confirmation Basis, Anchoring, Hindsight bias, etc. While, it is very difficult to avoid succumbing to these biases, it is worthwhile to keep a list of all these biases in front of oneself while evaluating investment decisions.

Economists Daniel Kahneman and Amos Tversky developed the concept of Prospect Theory in 1979 after an empirical study of the how individuals choose between alternatives in the presence of risk.

Prospect Theory is a very useful framework to describe how investors respond to gains and losses in the markets. In the most simplistic form, prospect theory can be described by the function shown in the graph above. It states that the pain felt by individuals when they incur losses is twice the pleasure felt when they secure gains.Applied to the field of investing, the theory states that investors value gains and losses differently, i.e. the emotional impact of losses is much higher than the emotional high of gains.

When it was formulated, Prospect Theory was completely against the prevailing consensus of the time, viz. economic agents are rational and treat losses and gains equally, and try to maximise their potential gains in all decision making. Prospect theory states that the emotional impact of potential losses causes significant changes in investor behaviour and thus affects decisions to buy and sell, and hence future returns.

Further research based on Prospect Theory has revealed a number of behavioural biases, which affect economic returns. We shall cover some of these in future posts. An awareness of these biases will help to prevent very obvious errors in investing, such as Confirmation Basis, Anchoring, Hindsight bias, etc. While, it is very difficult to avoid succumbing to these biases, it is worthwhile to keep a list of all these biases in front of oneself while evaluating investment decisions.

Friday, May 2, 2008

Well known value investors : Benjamin Graham is regarded as the father of value investing.

Benjamin Graham is regarded by many to be the father of value investing. Along with David Dodd, he wrote Security Analysis, first published in 1934. The most lasting contribution of this book to the field of security analysis was to emphasize the quantifiable aspects of security analysis (such as the evaluations of earnings and book value) while minimizing the importance of more qualitative factors such as the quality of a company's management. Graham later wrote The Intelligent Investor, a book that brought value investing to individual investors. Aside from Buffett, many of Graham's other students, such as William J. Ruane, Irving Kahn and Charles Brandes have gone on to become successful investors in their own right.

Graham's most famous student, however, is Warren Buffett, who ran successful investing partnerships before closing them in 1969 to focus on running Berkshire Hathaway. Charlie Munger joined Buffett at Berkshire Hathaway in the 1970s and has since worked as Vice Chairman of the company. Buffett has credited Munger with encouraging him to focus on long-term sustainable growth rather than on simply the valuation of current cash flows or assets.[7] Columbia Business School has played a significant role in shaping the principles of the Value Investor, with Professors and students making their mark on history and on each other. Ben Graham’s book, The Intelligent Investor, was Warren Buffett’s bible and he referred to it as "the greatest book on investing ever written.” A young Warren Buffett studied under Prof. Ben Graham, took his course and worked for his small investment firm, Graham Newman, from 1954 to 1956. Twenty years after Ben Graham, Prof. Roger Murray arrived and taught value investing to a young student named Mario Gabelli. About a decade or so later, Prof. Bruce Greenwald arrived and produced his own protégés, including Mr. Paul Sonkin - just as Ben Graham had Mr. Buffett as a protégé, and Roger Murray had Mr. Gabelli.

-Source (Web)

Graham's most famous student, however, is Warren Buffett, who ran successful investing partnerships before closing them in 1969 to focus on running Berkshire Hathaway. Charlie Munger joined Buffett at Berkshire Hathaway in the 1970s and has since worked as Vice Chairman of the company. Buffett has credited Munger with encouraging him to focus on long-term sustainable growth rather than on simply the valuation of current cash flows or assets.[7] Columbia Business School has played a significant role in shaping the principles of the Value Investor, with Professors and students making their mark on history and on each other. Ben Graham’s book, The Intelligent Investor, was Warren Buffett’s bible and he referred to it as "the greatest book on investing ever written.” A young Warren Buffett studied under Prof. Ben Graham, took his course and worked for his small investment firm, Graham Newman, from 1954 to 1956. Twenty years after Ben Graham, Prof. Roger Murray arrived and taught value investing to a young student named Mario Gabelli. About a decade or so later, Prof. Bruce Greenwald arrived and produced his own protégés, including Mr. Paul Sonkin - just as Ben Graham had Mr. Buffett as a protégé, and Roger Murray had Mr. Gabelli.

-Source (Web)

Thursday, April 3, 2008

Value investing - Finding an outstanding company at a sensible price rather than generic companies at a bargain price.

Value investing is an investment paradigm that derives from the ideas on investment and speculation that Ben Graham & David Dodd began teaching at Columbia Business School in 1928 and subsequently developed in their 1934 text Security Analysis. Although value investing has taken many forms since its inception, it generally involves buying securities whose shares appear underpriced by some form(s) of fundamental analysis. As examples, such securities may be stock in public companies that trade at discounts to book value or tangible book value, have high dividend yields, have low price-to-earning multiples or have low price-to-book ratios.

High-profile proponents of value investing, including Berkshire Hathaway chairman Warren Buffett, have argued that the essence of value investing is buying stocks at less than their intrinsic value. The discount of the market price to the intrinsic value is what Benjamin Graham called the "margin of safety". The intrinsic value is the discounted value of all future distributions.

However, the future distributions and the appropriate discount rate can only be assumptions. Warren Buffett has taken the value investing concept even further as his thinking has evolved to where for the last 25 years or so his focus has been on "finding an outstanding company at a sensible price" rather than generic companies at a bargain price.

High-profile proponents of value investing, including Berkshire Hathaway chairman Warren Buffett, have argued that the essence of value investing is buying stocks at less than their intrinsic value. The discount of the market price to the intrinsic value is what Benjamin Graham called the "margin of safety". The intrinsic value is the discounted value of all future distributions.

However, the future distributions and the appropriate discount rate can only be assumptions. Warren Buffett has taken the value investing concept even further as his thinking has evolved to where for the last 25 years or so his focus has been on "finding an outstanding company at a sensible price" rather than generic companies at a bargain price.

Subscribe to:

Comments (Atom)